![]()

| First Principles of Valuation The Valuation of Stranded Costs The Estimated Value of Stranded Costs in the Electric Utility Industry Other Elements of the Stranded-Costs PuzzleOther Elements of the Stranded-Costs Puzzle Stranded Costs and Economic Efficiency Efficiency and the Cost of Capital |

One of the main topics of concern facing the analysts of deregulation is the question of the so-called stranded costs. The term "stranded costs" has emerged as an issue only in the context of electricity deregulation. It has no roots in economic theory. For instance, there was little or no attention paid to stranded costs in the discussions on airline deregulation, trucking deregulation, and most oddly, the breakup of AT&T. note 1 Why the issue appears now and not in the first cases of deregulation is an interesting question, but one we leave unanswered here. Even so, the fact that there is little intellectual history is revealing. Indeed as most proponents of stranded cost recovery indicate, the main issue is equity and morality, not economics and efficiency. Some analysts have tried to make stranded costs into an economic issue, but as we demonstrate below, their arguments do not bear close scrutiny. What are stranded costs, and why have they received such scant treatment in the economics literature? A general definition is that they are any investment that will be less valuable under competition than under regulation. Two of the academic writers on this topic say that stranded costs are "those costs that the utilities are currently permitted to recover through their rates but whose recovery may be impeded or prevented by the advent of competition." note 2 Notice the choice of the term "utilities" and not "firm." The definition used by these authors, in and of itself, reveals the narrow focus of the topic. The term and concept of stranded costs have appeared and are used only in the context of electric utility deregulation. Consider an example from the telephony industry. In the early and middle 1970s, MCI and AT&T invested substantial sums in the installation of microwave towers which were rendered nearly valueless by the technological advance of fiber optics cable as the FCC deregulated the long-distance telephone market. Indeed, Sprint showed footage in its television advertisements of microwave towers being dynamited. Yet there was no hue and cry for recovery of stranded towers when the FCC deregulated the long-distance market. The functional definition of stranded costs compares the value of a firm’s assets in the regulated environment with the value of these same assets in competition. In the regulated regime, investor-owned public utilities are allowed to make a so-called "fair" rate of return on their prudently invested capital. In practice, regulators set the price of electricity so that the utility receives enough income to pay its bill plus the return of its fixed investments. In effect, historical or accounting costs of installation determine the current market value of capital. Regulators adjust the revenue stream up or down to insure that public utility operators earn the approved rate of return on the book value of capital. Under competition, a firm builds a plant on the expectation of future income and cash flow. The hope of this future stream of income motivates the investment. Once the investment is in place, and assuming that it has no alternative or salvage value, its economic value is determined by the future cash flows. A simple example will help to elucidate the principle. A firm is contemplating the construction of a facility. The firm expects that it can generate $100,000 per month of gross sales using this facility. Labor, materials, taxes and other inputs are expected to cost $75,000 per month to operate the facility. This leaves the firm with $25,000 of net cash flows after all its operating bills are paid. If the underlying capital investment will have no alternative uses once in place, its capital or market value is the present discounted value of $25,000 per month as far into the future as the situation is expected to exist. For purposes of the example, let’s assume that the facility and the sales and costs are expected to continue for 10 years, 120 periods. If the appropriate discount rate on these cash flows is 12 percent per year or 1 percent per month, then the market value of this capital in place is given by the formula: The decision to build the plant is transparent in this simple example. If the firm can construct the plant for less than $1.74 million dollars then it is a good investment, that is, a positive net present value project. note 3 The cash outlays on capital to construct the plant, if they are less than $1.74 million, are dominated by the expected value of the future net cash flows. If the firm makes the investment, under this scenario, the equity value of the firm will increase by the differential between the cash outlays on construction and the present value of the future expected net cash flows. Assume that the plant can be built for $1 million. What is this plant worth? There are two basic ways to answer this question. One is to place a historical value on the costs of putting the asset in place. Call this the historical cost accounting method. The cost accounting method says that the value of the plant is the accounting dollar cost of building the facility. Accordingly the plant is worth, and is carried on the books of the company, as $1 million of assets. Alternatively, there is the discounted cash flow or net present value approach. This valuation approach is based on the idea of efficient capital markets. It asks, what could the asset be sold for? Since the value of the expected net cash flows is $1.74 million, economic theory argues that in an efficient capital market a buyer can be found who will pay this sum. In this world, the plant is worth its market value, which is $1.74 million. Let’s take this scenario down the road five years. First, assume that the cash flows have accrued at the expected rate and that there is no change in expectations about the gross income or costs over the remaining five year life of the facility. Second, assume that based on the appropriate accounting rules the facility has been depreciated linearly at an annual rate of 10 percent over the 10 year life. What is the plant now worth? In accounting terms, the plant is worth its original cost of $1 million minus its depreciation, which is five times 10 percent or 50 percent. The current value of the plant for accounting purposes is $500,000. However, in value terms the plant is worth the net present value of the future cash flows. There are five years left of production where the facility produces a net income of $25,000 per month. The present value of $25,000 a month for five years at a discount rate of one percent per month is:

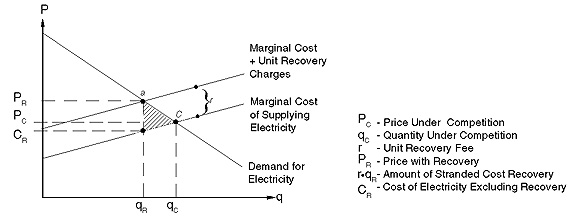

At the end of five years, the net present value of the expected future cash flows is $1.12 million. note 4 In sum, the accounting approach says that the plant is now worth $500,000 and the valuation approach says that the plant is worth $1.12 million. To understand the nature of stranded costs, now imagine that the expected revenues from the plant fall dramatically. Suppose the output of the plant declines significantly in price. Adjusting for this price change, the gross revenues fall to $75,000 per month. Costs also fall but not as much; assume they are now $70,000. note 5 The net cash flow to this enterprise is now $5,000 per month instead of the original $25,000. The present value of this sum for the remaining five years is $224,775. The plant which originally cost $1 million to build and which is being carried on the accounting books as having a value of $500,000 is now only worth $224,775 in the marketplace. The market value of the plant has plummeted because the price of its output has gone down. The Valuation of Stranded Costs Having gone through this exercise, we are now in position to be precise about the definition of stranded costs. Consider Table 7 where the preceding discussion is depicted and the so-called stranded costs are computed. The stranded costs are computed as the difference between the current market value of the asset in its productive employment and the historical cost of the asset depreciated through time using the approved accounting depreciation schedule. It is important to recognize that we have built this scenario upon the assumption that the capital has no alternative uses nor any salvage value. It is worthless for any purpose except the production for which it was built. And now this product has a lower price than anticipated. The fair market value of the asset is less than its accounting or book value. Its market value is now $224,775. On the books its appears to be worth $500,000, so it appears that the owners have lost $275,224. These are the stranded costs. In a free and open economy, this capital value loss is borne by the owners of the business. The market value of the company declines from $1,123,786 to $224,775. Based on market valuation, they lose $899,101. Their wealth is lower, but nothing else changes. Since, by construction, the plant has no alternative uses, production cannot be shifted to other products. At the same time, since it has no salvage value, it costs nothing in the opportunity sense to operate the facility. Any income generated in excess of the variable operating costs is paid to the owners of the business. The owners, although they are now poorer, are richer by running the plant than idling it. This is also revealed in Table 7 by an inspection of the last two rows. If the business is abandoned at any point in the ten-year period, the company has no equity or market value. If, at the five year point, the original revenue estimates hold and the facility is operated, then the equity value is $1,123,786. If, at the five year point the new revenue stream exists and the facility continues to operate, then the equity value is $224,775. Under any scenario, the company is worth more money if it continues to operate the facility. An important distinction is created. Financial losses are one matter, continued viability and operation of an enterprise another. Stranded costs can never be so large as to force the shutdown of a business. So long as the capital value of the business is positive, it pays the owners to operate the facility. Said another way, so long as gross revenues exceed current operating costs, it pays the owner to operate. To repeat, no facility will be abandoned or idled because of its sunk or stranded costs. At least that is the conclusion of basic economics and the modern theory of finance. Table 7 shows the calculation of stranded costs based on the difference between the fair market value of assets and their accounting or book value. This same methodology can be applied to the electric power industry. The Estimated Value of Stranded Costs in the Electric Utility Industry The first and most important point to note when we assess stranded costs in the electric utility industry is that stranded costs are not stranded productive facilities. As is clearly revealed by the foregoing analysis, stranded costs are an accounting and financial issue, not a production question. On the production side, capital in place with no alternative economic use will be productively employed so long as the price received for its output is at least as large as its marginal operating cost. All of our forecasts of the competitive equilibrium have market price above the marginal operating cost for additional production and the average total cost of operating and maintaining the facilities. The conclusion is that there will be few if any stranded production facilities due to deregulation. At the end of 1994, the book value of the firms in the electric power industry was around $400 billion. This is comprised of the historical cost of physical capital net of depreciation. This is the equivalent of the $500,000 number in the example in Table 7. In the real world, book value is complicated by capital structure that includes debt and preferred stock in addition to common equity. Book value of equity in investor owned utilities was $188 billion in 1994, long-term debt was $183 billion, and preferred stock made up the difference. At that point in time, the market value of common stock in the industry was $210 billion. The ratio of the market value of equity to its book value was 1.12:1. Unlike the example in Table 7, this says that for the industry taken as a whole the difference between market value and book value is positive. Table 7 reports the market to book ratios for various investor-owned utilities for 1993 through 1995. Using the most recent data, there are but seven firms with equity values less than their book values. These are Centerior Energy, Central Maine Power, Central Vermont PSC, Entergy Corp, Long Island Lighting, NY State Elec. & Gas, and Niagara Mohawk. To reiterate the argument we presented in the context of Table 7, true stranded costs are the fair market value of a firm’s assets minus their historical, depreciated book value. If the book value is greater than the fair market value, then the firm has stranded costs. If the fair market value is greater than book value, then the firm has no stranded costs. In the electric power industry, the book value of assets (for equity holders) is $188 billion. To determine the value of true stranded costs, we need an estimate of the value of assets in the electric power industry as they would be priced if the electric power market were fully competitive. While the current stock market valuation of equity in the electric power industry is not itself an estimate of the industry’s fair market value in competition, it does contain information about that valuation and about the level of true stranded costs in the industry. By all accounts, the financial community became keenly aware of the immediate possibility of deregulation and competitive pricing in the electric utility industry during 1994. Table 8 shows the stock prices for the firms in the industry. We have examined the detailed stock market reaction to several news stories during the year. note 6 On at least two occasions, news stories directly related to competition in electric power were met with sharp declines in the stock prices of investor-owned public utilities. These events are striking because of the near universal decline in industry stock prices in spite of the fact that these events related directly to only a couple of utilities. Over the entire year, equity value in the electric utility industry fell by 19 percent from around $260 billion at year end 1993 to $210 billion at the end of 1994. This caused the ratio of market equity value to book equity value to fall from 1.39:1 to 1.12:1. However, in spite of this decline in market equity, which can be reasonably related to a market perception of declining prices of electricity into the future, the market value of equity was still higher than the book value for the industry as a whole. Throughout 1995 the stock market continued to react to news of deregulation in the industry and to economy-wide and world-wide events that implied changes in the cash flows of electric utilities. Overall, stock prices in the electric utility industry rose in 1995 by nearly as much as they fell in 1994. However, this did not occur uniformly across the industry. The stock price of some firms fell in 1995. Notably, Niagara Mohawk had an equity value decline of 25 percent in 1994 and 58 percent in 1995 for a two-year return of -68 percent. On the other hand, some firms regained in 1995 all that they had lost in 1994 and more. For instance, the Southern Co. only lost 4 percent in 1994 and gained 21 percent in 1995. There has been substantial diversity in the stock price movements of the firms in the electric utility industry since the advent of competitive pricing initiatives. This diversity is understandable because the effects of competition will not be evenly distributed across the industry. Arguably, the stock market’s response to the news events of deregulation is muted. In other words, the stock market is valuing the common equity of investor-owned utilities based on a chance of deregulation, but the chance is less than one. The stock market has responded only partially to the threat of deregulation and falling prices. Until an event like deregulation is actually completed there is always some chance that it will change in form or be completely abandoned. The expectation of different possible outcomes has to be accounted for in the prices of the financial securities. From the perspective of the researcher or analyst, it is difficult to assess precisely the subjective probabilities employed by the financial market in arriving at the current stock price. However, there are certain principles that apply. First, the current stock price is an estimate of the fair market value of the firm in competition, the value of any non-utility assets, and the probability of the recovery of stranded costs either by explicit payment or by delaying the move to competition. note 7 In a regulated environment, the firm is allowed to collect revenues above operating costs to pay off its invested capital with an approved rate of return. Assets that are productive but fully depreciated recover only their operating costs. The firm’s equity value should equal its book value. In a competitive regime, the fair market value of the firm depends on the cash flows produced by the firm’s assets as shown by our analysis in Table 7 above. Some fully depreciated assets, worth essentially nothing to stock holders in a regulated environment, are worth substantial amounts in competition because their operating costs are below the price of output. In the move to competition, the firm’s equity value can be either above or below its book value depending on the net cash flows provided by its assets. In addition, the firm’s current equity value includes the possibility that in the move to competition, regulators will allow the firm something extra, something in addition to a pat on the back as the firm walks out the door into the world of competition. There is the chance that regulators will allow the firm to recover part, all, or even more than the firm’s true stranded costs (where true stranded costs are the difference between the fair market value of its assets and their book value). Most observers seem to think that regulation will allow partial but not full recovery of stranded costs. In the extreme, if the financial market feels that there will be no stranded cost recovery, then the current stock price is equal to the fair market value of the firm’s assets in competition. If the financial market feels that full recovery will occur, then the current stock price can be no larger than book value if there are true stranded costs. Finally, if the financial market feels that firms will get more than true stranded costs, then the current stock price can be larger than book even if the fair market value of the firm is less than book. If the financial market expects that there will be a recovery of stranded costs based only on the difference between the fair market value of the assets of the utility in a competitive regime and their undepreciated book value, then the current stock price is an unbiased forecast of whether stranded costs exist. Under this assumption, stranded costs only exist if fair market value is less than book and even if all stranded costs are recovered, equity value can never be bigger than book. If price is below book, the market is predicting that the fair market value of the firm’s assets in competition is worth less than book. If the financial market expects that there will be nothing more than the recovery of true stranded costs, then only firms with current market-to-book ratios less than one have any true stranded costs. If the market expects that firms will get something but no more than true stranded costs, the market applies the expectation of this likelihood to the current valuation. The financial market factors its subjective probability of the recovery of true stranded costs into the stock price. For instance, assume that Niagara Mohawk, which currently has the lowest market-to-book ratio in the industry, will have no equity value in a competitive regime. It will likely go bankrupt without some recovery of stranded costs. Its 1995 year-end equity value of $983 million is, then, based on the expectation that it will be allowed to recover some stranded costs. If its fair market value is zero, then the market to book ratio is the financial market’s forecast of the probability of the recovery of stranded costs, that is, 39 percent. If we use this as the expectation of the probability of stranded costs recovery across the industry, we can calculate the financial market’s estimate of stranded costs based on the assumption that firms will not be allowed to recover more than true stranded costs. If the financial market thinks that only true stranded costs will be recovered, then only the firms with market to book ratios less than one have stranded costs. From this analysis we have stranded costs as follows: Centerior, $1.2 billion; Central Maine Power, $28 million; Central Vermont PSC, $365 million; Entergy, $321 million: Long Island Lighting, $563 million; N.Y. State E & G, $171 million; and Niagara Mohawk, $2.5 billion. The total financial market estimate of stranded costs across these seven firms is $5.1 billion, and using the market to book definition of true stranded costs, none of the other firms in the industry has any stranded costs. This is not a very big number compared to the amount of stranded costs estimated by others. Maybe it is small because the financial market thinks that utilities will get more than true stranded costs. Let’s examine this possibility. If utilities are allowed to get more than the book value of their assets minus the fair market value of them, then the current equity value can be larger than book value. For instance, if utilities are paid the full book value of their assets as stranded costs, which is around $188 billion, and if they get to keep their assets which are still valuable, then the current stock price will include the excessive stranded cost recovery plus the fair market value of the assets. If this is true, that is, if the financial market thinks that some firms will be able to recover more than their true stranded costs, we can still draw an estimate of the true stranded costs. It depends on the expectation of the probability of excessive stranded cost recovery and on the extent of excess. Our best forecast of true stranded costs under the assumption that there will be excessive stranded cost recovery is that true stranded costs are around $21 billion. Some firms in addition to the seven listed above enter the group—Consolidated Edison, Northeast Utilities, Pacific Gas & Electric, and Edison International, to name a few. The additional firms have market to book ratios slightly higher than one, but true stranded costs are confined to firms with market to book ratios not far from one. In the final analysis, the financial market seems to be saying, in spite of the rhetoric, the true value of stranded costs is not very high. Finally, it must be noted that we are not factoring long-term debt into this analysis. It may be the case that the current equity value of these firms is based on some expectation that in bankruptcy the old equity holders will not lose everything. It is true that the bankruptcy process produces this result as a commonplace. note 8 However, the returns to old equity holders going through bankruptcy are not large and are not significantly inflating the equity value of the electric utility industry. It is easy to get confused about bankruptcy and financial distress. In and of itself, bankruptcy is a financial outcome. The wealth of the old equity owners is exhausted, and the debt holders usually recover less than full value. However, the physical capital and labor pool is neither destroyed or directly affected by the financial reorganization. Later in this chapter we discuss several bankruptcies that have already occurred in this industry. It is enlightening to forecast the effects of the possible bankruptcy of a few firms due to deregulation from the experience of the firms that have already gone through it. The fact that the old equity holders lose substantially all of the wealth they had invested in the assets has no bearing on the productivity of the women, men, and machines comprising the operating unit. Whatever the inputs could do before bankruptcy, they can still do afterwards. Bankruptcy does not change the stock of human or physical capital. We do not predict massive bankruptcies to follow from competition. The few that may occur will actually be efficient reorganizations that make for smoother operations in the future. This is the focal point of our analysis. The debate surrounding stranded costs tends to obscure the real issues. The assets of the electric power industry are not idled by the fact that the movement to competition makes some of them less valuable in a financial sense. Independent of the recovery of stranded costs, in a competitive market for electricity, the fair market value of productive assets will be determined by the difference between market price and production cost. If market price is larger than average production cost for an asset, then it will be employed. It will have market value, quite possibly market value in excess of its book value. But regardless of whether its fair market value is larger or smaller than its book value, it will be productively employed. Other Elements of the Stranded-Costs Puzzle There is a second category of stranded costs. Many utilities have contracts to buy power at rates that are higher than the forecasts of prices under competition. These purchase power contracts whether voluntary or mandatory are analytically identical to the physical capital problem just described. The contracts mandate a minimum amount of power to be purchased at a pre-specified price. The capital value of these contracts rises and falls with the price of electricity. Long term contracts are akin to options. For example suppose a power company has a contract to buy one million kwh of electricity per year for the next ten years from some supplier at a price of 12 cents per kwh. Let the current price of power be 12 cents. Then this contract has no economic value. The spot price of power and the long-term contract price are identical. note 9 Now imagine that the spot price of electricity increases to 13 cents per kwh. Then the rights to purchase power at lower than market rates have positive capital value to the buyer. The present discounted value of the difference between the spot and contract prices times the allowed quantity over the life of the contract is the capital value of the contract. The value of the contract becomes negative to the buyer (the electric utility) if the spot price or the expected spot price declines below the contract price. The present value of the difference between the contract price and the current price, times the required purchase volume will be the change in capital values accruing to firms with these purchase contracts outstanding. Firms with large volume purchase contracts at prices higher than anticipated under competition will sustain value losses when the price declines from its current regulated levels. This price decline is a second source of stranded costs. It is noteworthy that the bulk of the contracts with high purchase prices and negative capital values appeared as a result of PURPA of 1978, and they are most prevalent in New York and California where public utilities were required by regulators to enter into these contracts for purchase. In the current system, utilities are allowed to charge rates that are sufficient to pay the costs of their purchased power as an operation expense. In a world of freely competitive prices, rates will become unrelated to these pre-existing long-term purchased power contracts. The negative capitalized value of these contracts can be called a stranded cost. note 10 Stranded Costs and Economic Efficiency We are left with the question, Why is so much made of stranded costs in the case of electric utilities? Essentially there are two answers. First, one group of analysts claim that there was some compact or contract created by the public regulation of utilities. Of course any such compact was and is implicit. No formal contract exists. But leaving that question aside, what is the nature of this compact? Essentially, electric utilities agreed to sell their output at prices determined by governmental regulators instead of market forces. They also agreed to sell the desired demand for power at the regulated prices, and they agreed to supply power in their designed service area to all buyers in that market regardless of the cost of connection and service. In exchange, the utilities got freedom from competition, the right to recover their variable costs, and the right to make a "fair rate-of-return" on their prudent investments. According to the compact theory of regulation, the electric utilities should be allowed to recover all of their stranded costs. Otherwise the state has reneged on its leg of the bargain. Most any casual reading of the Declaration of Independence or the United States Constitution suggests that there is a compact between the citizens and their government. If so, then an alleged compact between electric utilities and government is not special or deserving. All citizens have a compact, not just the owners of electric utility stocks and bonds. Any compact is a two-way deal. Producers and consumers were supposed to get competitive prices as part of the bargain. Whether any implicit one-way compact or contract with electric utility investors ever existed is a matter of individual opinion. But we can note that if the compact theory applies, then the debt of public utilities should have the same risk level as government bonds. This is because under the one-way compact theory, government cannot take action that decreases the net revenue stream required to maintain the approved rate of return. Even a superficial analysis of bond prices and yields reveals that electric utility debt has a higher return, implying higher risk, than comparable, risk-free government securities. This implies that the holders of this debt believe that there is at least some chance that any one-way compact between government and regulated firms is not inviolate. Table 9 shows the yields to electric utility and government bonds for several different points in time. Note that the electric utility yield is always higher, implying greater risk. Under the compact or contract theory of regulation that allows for complete recovery of stranded costs, the difference should average zero, but it does not. The existence of this risk premium for electric utility bonds shrouds the compact theory in darkness. Were there a true contract between government regulators and electric utilities, all the default risk of the bonds would vanish. As the data reveal, it has not. While there may have been some sort of conceptual understanding or deal between regulators and utilities, financial investors did not view the deal as risk free. And well they shouldn’t. There have been a number of financial failures in the electric power industry both for investors in privately-owned and publicly-owned utilities. We discuss these in some detail below as regards the effect of bankruptcy and default on the operation of the physical facilities. The point here is that if the regulatory compact ever existed, it has been routinely violated in the past as evidenced by the financial failure of a number of prominent utilities. If there is a one-way regulatory compact, why have holders of Washington Public Power Supply System bonds not sued for recovery of their financial investment stranded by the default of these securities? Let’s return to our second answer to the question, Why is so much made of stranded costs in the case of electric utilities? As we have pointed out in detail above, stranded costs cannot, by themselves, idle or render unusable any facility. However, some analysts question the effect of stranded costs on the expansion or contraction of capital in the industry. For instance, some have argued that the inability of electric utility firms to recover their stranded costs will spill over to the quality of their debt and lead to a downgrading in bond ratings. According to this argument, the lower quality bonds raise the cost of capital to the industry, and this is bad. This line of argument is a ruse. At any moment in time there is uncertainty about the future value of electricity to consumers. The consumption value of electricity can rise or fall as progress unfolds and invention changes the structure of relative prices. That risk can be distributed across a wide variety and classes of individuals. In the simplest case, the seller of the product bears all the risk of price and cost changes. Customers come and go as the price varies. In more complicated scenarios, sellers can arrange long-term contracts with buyers that shift some of the uncertainty to the purchasers. In the case of electricity, since sellers are allowed to recover all of their prudent costs, a significant portion of price and cost variability has historically been placed on the shoulders of consumers. Shifting this risk back to producers does not, by itself, change the underlying structure of uncertainty. The important point to keep in mind here is that capital costs have been too low for producer investors. The opportunity cost of capital includes all the inherent risks, and by virtue of the existing regulations, the opportunity cost to investors has been too low. However, there is actually a positive benefit of shifting the risk to producers. They are better equipped to manage the risk. First, the electric utility investors can diversify their financial holdings across a broad spectrum of assets and thereby eliminate any systematic risk unique to electricity production. While consumers might engage in a similar strategy, it is more costly for them. Second, producers are in better position to anticipate and manage inherent risk than consumers. In order to deal efficiently with fluctuating electricity prices, consumers would have to individually arrange for alternative fuels for heating, lighting, and the like, or purchase the proper financial portfolio. However, by virtue of their relatively small purchase volumes, these alternative, diversification options are very costly. The issue boils down to the question, who is better able to bear and manage risk: working families or electric utility risk managers? Some utilities that have disproportionally large stranded costs may be forced into bankruptcy if prices in their markets were to fall to competitive levels. Will the financial difficulties of these utilities preclude the delivery of reliable electricity? Our review of the past experiences of financial distress in this industry lead us to answer this question in the negative. The fact that insolvent utilities remained viable producers of electricity both during and after financial restructuring suggests that electricity customers will not be harmed by any wealth losses visited upon utility investors. Some perspective on this question can be gained by examining the history of reliability and financial distress. NERC has reported no problems in reliability in the past two decades. Yet over the same time, a handful of utilities have undergone extended periods of financial distress. Most of these difficulties are related to investments in nuclear power. In April of 1984, the Wall Street Journal reported that three utilities, Public Service Company of New Hampshire, Long Island Lighting Co., and Public Service Company of Indiana (PSI), "are being pushed toward seeking court protection from creditors." PSI was taken off the hook for its $2.5 billion dollar investment in the canceled Marble Hill nuclear plant by the Indiana regulatory commission. The other two firms had long, drawn out experiences with the threat of bankruptcy, which are detailed below. The most notable recent example of financial distress is Public Service Company of New Hampshire (PSNH). PSNH was the lead partner in the construction of the Seabrook Nuclear Power Generator. Seabrook was a troubled project from the beginning, which can be marked as the application for a construction permit in early 1972. Permits and plans were repeatedly delayed, approved, suspended, and reinstated during the mid-1970s; ground was finally broken in August, 1976. Nevertheless, groups opposed to the plant or various aspects of it continued to win court injunctions and stays that had negative implications for the financial viability of the project. Financing difficulties halted construction of the first reactor in 1984 and caused a second to be canceled. The initial expected cost of Seabrook was $1.0 billion; by the time it was completed in 1989, the total was $6.3 billion. Forbes magazine called Seabrook "the largest managerial disaster in business history." The expense, coupled with the protracted delay in revenue from power generation produced a river of red ink for PSNH and its partners. Numerous maneuverings in 1979, including an emergency rate increase, sales of stock, and rearranging of credit lines signaled trouble. That PSNH might be forced into bankruptcy was openly discussed at least as early as 1982. In 1984, additional moves including the omission of dividends and conversion of missed payments to loans forestalled formal bankruptcy proceedings temporarily. PSNH filed for bankruptcy in January of 1988, the first investor-owned utility to do so since the 1930s. It did not emerge from bankruptcy until May of 1991, under a plan which involved a subsequent merger with Northeast Utilities. The merger was finally completed in June, 1992. The period of financial distress for PSNH lasted over a decade. In spite of this, there was no idling of any productive facilities of PSNH. A second utility, El Paso Electric (EPE), filed for bankruptcy in September, 1992. EPE’s troubles stemmed from is 15.8 percent share of the Palo Verde Nuclear project. Signs of financial trouble begin in 1986. Standard & Poor’s placed the company on its credit-watch list in February and lowered the debt rating from BBB to BBB- in September. In 1987, EPE requested a 33 percent rate increase, and Standard and Poor’s lowered the rating to BB+. EPE sold its stake in Palo Verde for $250 million in 1988 in a lease-back arrangement, suspended the common stock dividend in 1989, sold additional assets in 1990, and reported its first loss of $105.8 million. By January of 1992, EPE was not expected to avoid bankruptcy. It had survived because its creditors granted "extension and waivers." It filed for Chapter 11 in January 1992. Two serious merger proposals ultimately failed, and the reorganized company emerged from bankruptcy protection in February 1996. Again, from the production side, bankruptcy did not cause any power plant to be idled. The third case is Long Island Lighting Co. Long Island Lighting’s financial troubles stemmed from its investment in Shoreham, a nuclear plant that was built and decommissioned without producing a flicker of power. In 1983, Moody’s downgraded all of LILCO’s debt, much of it to speculative rank. Layoffs, salary cuts, and dividend cuts were implemented in its battle to survive the costs of its Shoreham nuclear power plant. The utility appeared to be on the verge of bankruptcy several times in 1983 and was rescued by extension of default deadlines by major lenders and an annual rate increase of $245 million that the Public Service Commission explicitly stated would enable utility to obtain bank financing it needed to stay solvent. Dividends on common stock were not restored until September 1989. In 1989 LILCO was poised to obtain a license to begin production at Shoreham when it agreed to decommission the plant in exchange for billions of dollars in rate increases. The rate hikes granted in the interest of keeping LILCO solvent forced its customers to pay the highest electric rates in the country. Residential customers paid 16.8 cents per kwh in 1994, roughly twice the national average and 50 percent above those in the New Jersey and Connecticut suburbs of New York. LILCO survives in its current form only because its customers—who are searching for ways to purchase from alternative sources—have been saddled with billions of dollars in Shoreham expenses. The infamous 1979 Three Mile Island accident created substantial financial distress for its owner General Public Utilities. GPU faced massive losses as a result of the disaster. Clean up costs alone were projected to be enormous. Yet the most immediate problem stemmed from the loss of two revenue producing assets—the damaged reactor and an undamaged reactor (unit #1 which did not return to production until management issues were resolved in October 1985). Immediately following the accident, the firm sought $450 million in bank credit to avoid bankruptcy. Shortly thereafter a cooling system problem at the Oyster Creek Nuclear Station shut this plant down for the month of May. Yet the lights stayed on. The firm drew additional power from its other generating facilities and negotiated contracts to purchase electricity with Philadelphia Electric, Pennsylvania Power and Light, and Ontario Hydro. To solve to its financial hemorrhage, GPU turned repeatedly in the following years to the utility commissions of New Jersey and Pennsylvania for rate increases, approval to pledge accounts receivable as collateral for bank loans, and other emergency measures. Stock dividends were eliminated and did not resume until April 1987. There has even been a Savings & Loan related failure in the electric power industry. Tucson Electric Power (TEP) Co’s troubles stemmed from a "stream of misdirected investments" in ventures unrelated to electricity. A new CEO in 1985 began an acquisition binge in auto financing, venture capital, real estate, and investments in thrift institutions that by the end of 1988 had swollen to nearly 40 percent of the company’s assets. The possibility that bankruptcy protection would be sought was raised in May of 1990. Auditors claimed the company could not stay afloat in April of the following year, and creditors attempted to force Chapter 11 proceedings in July. Financial restructuring was ultimately completed in December of 1992, although losses continued to plague the company in 1993 and 1994. Finally we have the default of a publicly-owned utility. The Washington Public Power Supply System (WPPSS) was organized in 1957 for the purpose of developing electric power generating facilities. WPPSS originally consisted of 17 municipal electric utilities. WPPSS and the Bonneville Power Administration (BPA) made ambitious plans to develop as many as twenty nuclear power plants to serve the Pacific Northwest region. The first project, begun in 1971, was to build three plants at an expected cost of $1.6 billion; these costs were to be shared by 105 municipal utilities and five private utilities involved as partners. In 1976 most of these same utilities combined to build two additional plants. This was somewhat out of step with national trends. By 1974, dozens of nuclear projects outside of the Pacific Northwest had been canceled, and a greater number were being delayed. In 1981, a review by the budget director projected the total cost of the project to be $23.8 billion. Work on the second batch of plants was terminated. Eventually, two of the three original plants were mothballed; only one plant was ultimately completed. Court rulings invalidated the contracts signed by some of the municipal utilities to finance the second batch of plants. As a result, WPPSS defaulted on $2.25 billion of debt in July of 1983, the largest municipal default in the nation’s history. Litigation over this default continued into the 1990s. Even so, it does not seem to have had led to a significant decline in the flow of capital to public enterprises. Financial difficulties are not a phenomenon of the 1990s for utilities. In 1970, S&P’s bond ratings were AA or AAA for 80 percent of the electric utilities. By 1981, there were none with AAA ratings and just 25 percent had a rating of AA. The idea that utilities represent the safest return one can obtain has long gone out the window. Typically, these troubles trace to investment in nuclear power plants. Investors lost big sums; electricity consumers lost even more. When in financial difficulty, utilities with nuclear investments repeatedly requested and received rate increases from the state public utility commissions. Even before the massive cost overruns had taken place, the finance director of the Public Utility Commission in New Hampshire found that the generating capacity (PSNH) proposed for Seabrook was not needed and would unnecessarily raise the electricity bills of New Hampshire consumers. His report was ignored. The result of these decisions is a checkerboard pattern of electricity rates (New York, its neighbors, and the state of New Mexico are prime examples) whose only rationale is that one utility district made a nuclear investment and its neighbor did not. This would not stand in a competitive environment. According to our research, there is not a single mention of reliability problems related to these firms in the literature. Theory suggests that they would continue to produce electricity because the net revenues from continued operation are enormous. Production is their main source of net revenue. The stranded cost question may be in large part an issue of a few, select, imprudent nuclear power plant investments. The few, high-rate utilities that will be hurt by competition typically have big nuclear investments, some of which are not producing electricity. In general, nuclear power plants are efficient, but in several isolated cases, where the timing of investment was bad and where construction delays added to capital costs, some plants will simply never recover their original costs except by some regulatory fiat or other transfer of money from consumers or taxpayers. Denial of stranded costs would do much of what bankruptcy did in these cases, but history suggests that it would not shut off the power or reduce the willingness or capacity of the industry to invest prudently in the future. The preceding cases suggest that bankruptcy, while a nightmare for equity investors and bond holders, seems to have had virtually no impact on the smooth operation of the industry or the firms involved. The implication appears to be that any similar financial distress that may be created by deregulation will be absorbed by the industry in like manner. We forecast that deregulation will not dim light bulbs even if some investors lose money. note 11 Efficiency and the Cost of Capital If the apparent cost of capital does in fact increase for electric utility operators, it is actually efficient and enhances the operation of the economy. To the extent that capital investment decisions have been based solely on the portion of risk borne by investors, the cost has been artificially low. The end result has been excessive and imprudent investment in capital. Shifting the risk of capital solely onto the shoulders of producers eliminates this problem. note 12 With regulation and revenue recovery, the risk of changes in capital values is borne by electric utility consumers. With competition, this risk shifts to capital owners. The simple shifting of risk does not increase its magnitude or jeopardize the production and consumption in the industry. It simply redistributes the risk to different parties. Moreover, firms with the ability to manage and diversify risk via the share holding of their owners are far and away more efficient risk bearers than consumers of the product. On both counts, the economy is better off because efficiency is enhanced. Couple this argument with the fact that deregulation may well bring with it a strikingly different face associated with marginal capital expansion. If additional capital in the industry is provided by relatively small, relatively efficient gas turbine generators and if much of this generating capacity is owned by industrial users that provide power to the electricity transmission grid in conjunction with meeting their own energy needs, the riskiness of marginal capital investment in the electric power production is not identical to the riskiness of the currently invested capital. In sum, there is no efficiency argument in the cost of capital issue. Relabeling stranded costs as cost-of-capital does nothing to change the fact that it is mainly a distributional issue. The goal of regulation in general should be to make the economy work more efficiently in order to maximize the wealth of its citizens. For this goal to be achieved in the context of the electric power industry, lower bond ratings and higher interest rates for utility construction are not a problem but rather a benefit for the larger economy. On the Efficient Recovery of Stranded Costs Throughout the preceding discussion we lay the claim that from a scientific economic perspective stranded costs are normative not positive. Whether a firm recovers its stranded costs or not has no impact on its decisions as to what types of fuel to use, how much output to produce, what price to charge, what types of new investments to make, the appropriate level of maintenance, or any other operating characteristic. Any utility that is allowed to recover some or all of its stranded costs by regulatory fiat in the move to competition will experience a wealth increase. This wealth increase will accrue to equity holders in higher stock prices and to bond holders to the extent that the mandated recovery of stranded costs affects the utility’s bond ratings. However, these are merely questions of income redistribution so long as any stranded costs are recovered efficiently. Regulators in charge of the transition to open and free competition should be aware that, if they decide to allow the recovery of any fixed costs, they should do so efficiently. Basically there is but one efficient way to transfer funds from electric utility consumers to producers, and that is with fixed or access fees. Consider the graph represented in Figure 7.

The demand for electricity and the marginal cost of producing power are shown. note 13 Under competition, the price of power will be Pc. At that price, consumers will buy qc units of power per period. Now suppose that regulations are put in place so that under competition producers are allowed to recover some or all of their stranded costs via a unit increment of tax on power. Let this unit recovery charge be r. The price of electricity will rise to Pr, and the consumption will decline to qr. Notice that the price of electricity will only rise by the amount of the recovery charge if the marginal cost of supplying electricity is constant over the relevant range of output. The new, net-of-recovery charge payment to utilities for power falls from Pc to Cr (because marginal cost is rising and less total output is being produced). Those utilities that do not recover any of their stranded costs will see a lower market price for electricity. This will idle the facilities with the highest marginal costs of production, and as the graph confirms, total output will decline. The utilities will receive an extra rqr of revenue which will be called the stranded cost recovery. Some of this is just a transfer of consumer surplus to utilities that, leaving aside the rent-seeking costs created, will have no ill economic effects. However, as the graph reveals, there is a dead-weight loss to the economy engendered by the unit price recovery method. This dead-weight loss is the shaded area, Dabc, in the figure. A portion of this triangle is lost consumer surplus and a portion is lost producer profit. The lost triangle is the inefficiency of a unit charge recovery of stranded costs. The inefficiency does not arise from the fact that consumer surplus is transferred to producers. The inefficiency is created because the demand price for power lies above its marginal cost of production. Imposing regulation that stipulates that stranded costs are to be recovered by a per-unit fee, r, drives a wedge between the value of power to consumers and its cost of production at the margin. A potential gain from trade is denied. The worst example of this would be for regulators to tack the recovery fee onto transmission rates. There are no stranded costs in transmission, and bundling these two activities creates an inefficient cross subsidy. note 14 There is a simple way to avoid the dead-weight loss of stranded costs recovery which still allows for recovery. The efficient system uses access or lump-sum fees to transfer funds between consumers and producers. In effect, the price of electricity has two components. One component, the access charge, is for the use of the system. This charge does not depend on the amount of electricity purchased by any consumer. The other component is the unit charge. It bears noting that the move to competition in telephony has created this two-part scheme. Each telephone user pays a network access fee and then pays per minute charge for the long-distance calls. The access fee bears no relation to number or duration of long-distance (tariff) calls.

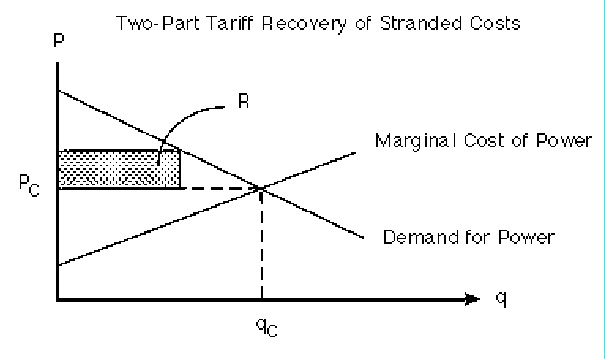

Figure 8 demonstrates the relative efficiency of two-part prices over unit-cost recovery. Again under competition and no recovery of stranded costs, the price of electricity will be Pc and consumption will be qc. Suppose there are n homogeneous consumers who create the demand for power. Then suppose that R is the amount of stranded costs that regulators have mandated that utilities be allowed to recover. The efficiency access fee is R/n per period per customer. Note that this has no impact on the unit price of electricity. Assuming that there are no income effects in demand generated by this access fee, then demand is unaltered. Some analysts have suggested that this two-part access fee will reduce the number of customers. This need not be the case. Each consumer who was previously purchasing power continues to purchase the same amount prior to the access charge. This two-part price allows for the transfer of funds from consumers to producers without affecting the market equilibrium. No doubt, the wealth of consumers is lower, but the wealth of producers is higher by an exact offset. This is just a transfer with no impact on operational efficiency, economic welfare, or gross national product. It simply is a transfer of wealth with no other consequences. An alternative to two-part tariffs is to use the general taxing authority of the state to provide the lost wealth. In other words, states could levy an income tax and pay these proceeds to the electric utilities to cover their lost income from lower electric prices. Of course, most any observer will immediately say, this is politically unlikely and poppycock. Therein lies its point. A two-part tariff for stranded cost recovery is nothing more than a consumption tax on electricity consumers. Neither a tax on electric consumers or a general tax has any operational implications for the electric power industry. Why one might be considered poppycock and the other a real prospect is an open issue. Given that almost all income-tax payers are also electricity consumers, the distinction nearly vanishes. The fact that a general tax and subsidy paid to the electric power industry to offset stranded costs smacks of corporate welfare does not change the color of the horse. It has been proposed that electric utility firms be allowed to charge "exit" fees when they lose their customers to rivals. While this system would indeed transfer income to these firms, it would do so inefficiently. If Firm A has a customer who wishes to do business with Firm B, but the exit fee prevents the change, then the customer and the economy is stuck with the higher cost producer, A, in lieu of the lower cost seller, B. Some analysts have incorrectly argued that exit fees are efficient on the grounds that Firm A has lower operating costs than B but higher fixed costs of operation due to some circumstance. They then make the mistake of arguing that firm A will lose the customer to Firm B. The higher non-marginal operating costs will not raise the price offered by Firm A. High fixed costs do not cause Firm A to lose rivals to Firm B. Only marginal operating costs determine price, at least in the short run. Even if the lower marginal operating cost firm, A, was forced to bankruptcy by its fixed obligations, its operating capital would reemerge, reorganized under new ownership. The financial reorganization would not alter Firm A’s inherent operating cost advantage. Partial Recovery of Stranded Costs There are proposals to allow some, but not all of stranded costs to be transferred to producers. For instance, if producers are efficiently allowed to charge consumers or taxpayers half of their stranded costs, then consumer welfare decreases by the amount of the stranded cost recovery. As long as this recovery is not based on unit price increases or transmission cost increases, there is no reduction in the net welfare gains from competition. Any stranded cost recovery based on access fees reduces consumer welfare by the amount of the stranded cost recovery but has no effect on net welfare. Our point here is simple but decisive. The decision to allow the recovery of sunk costs is a normative, political decision. Scientific economic analysis cannot be used to make the call on whether they should or should not be recovered because if they are not recovered, there will be no economic efficiency effect. However, if the process decides that stranded cost recovery is to be the rule of the day, then these costs should be recovered efficiently via a two-part, access-charge tariff or a general tax levy and subsidy that does not disturb the relation between the price of electricity and its marginal cost of production. Prudency We close our discussion on stranded costs with a brief discussion on prudent investments. Suppose that someone adopts the one-sided compact theory of electricity regulation and concludes that some recovery of stranded costs is mandated. Is it not then prudent to determine ex post which original utility investments were in fact prudent at the time? In many cases, consumers who are currently paying fees for inefficient capital investment, mostly nuclear plants, could have been served by their utility companies with purchased power. Why did the Public Service Company of New Hampshire and its regulators build Seabrook instead of contracting with other extant utilities to generate and transmit the power desired by PSCNH’s customers? Was it prudent for Pacific Gas and Electric to build the Diablo Canyon nuclear power plant when power might have been bought from other firms to satisfy consumer demand? If these firms and others similarly situated could have bought power instead of building plants, is it proper for their current customers to pay for the mistakes? Notes:

|